When a hurricane is brewing in the Gulf, most boaters focus their hurricane prep on tying down lines, pulling boats from the water, or finding safe harbor. What many don’t realize is that even the best preparation can’t always prevent damage, and when your boat ends up grounded, sunk, or drifting, the cost of getting it back can be shocking. That’s where “salvage” comes in, and according to Captain Joseph Frohnhoefer III, CEO of Sea Tow Services International, it’s one of the most misunderstood parts of boating insurance.

“Salvage is saving an object in peril at sea,” Frohnhoefer explains. “It could be a vessel, engines, electronics…anything in danger on the water.” The key phrase there is “in peril.” Under maritime law, once your vessel is in danger, whether from grounding, sinking, or drifting toward something that could destroy it, any effort to recover or save it becomes a salvage operation. That legal definition matters because it determines who pays and how much.

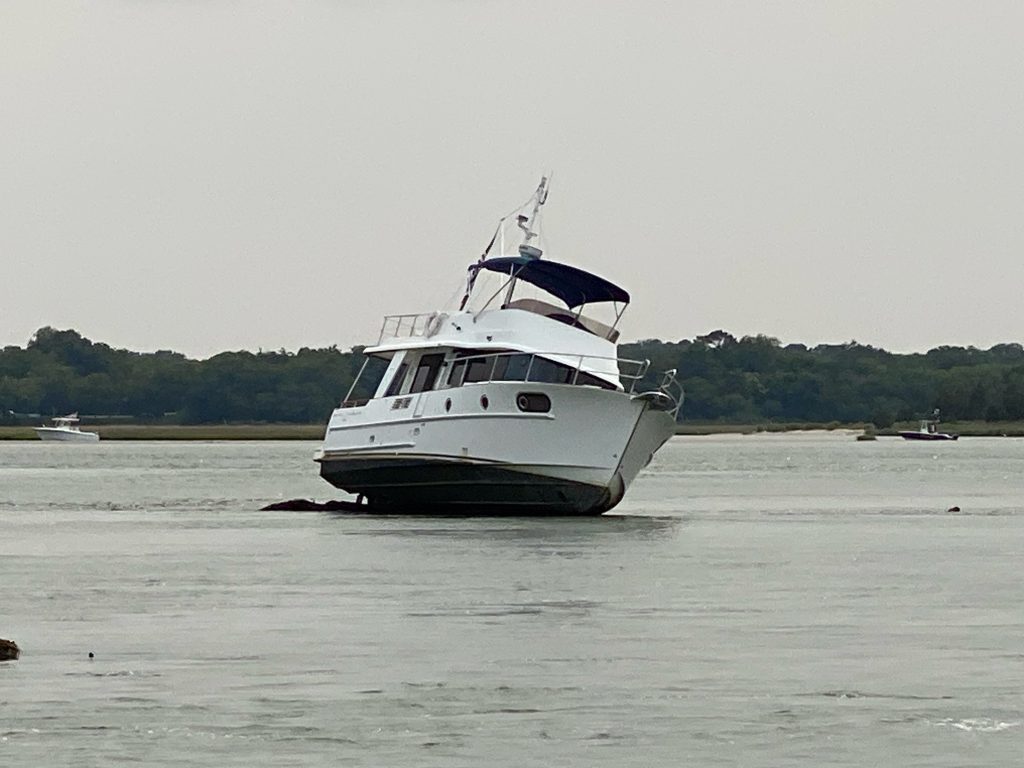

A Tow vs. A Salvage: The Line Between Calm and Catastrophe

Sea Tow is, first and foremost, a towing service. Membership provides peace of mind for mechanical failures, dead batteries, fuel delivery, and other routine breakdowns on calm days. But that coverage ends where true peril begins.

“Everything we do on the water is technically salvage,” says Frohnhoefer, “but the level of peril is what makes the difference.”

Here’s a simple hurricane prep example. If your boat breaks down on a clear, calm day and you drop anchor to wait for help, you’re not in peril. That’s a towing job; something covered by a Sea Tow membership. But if you break down in rough weather, lose power, and your boat starts drifting toward a jetty, you are absolutely in peril. When a Sea Tow captain responds, that rescue is no longer considered towing. It’s salvage. The crew may use the same boat and the same gear, but legally, the service falls under maritime salvage law. You’ll get a bill for that work, and your insurance company will either reimburse it or leave you paying out of pocket, depending on your coverage.

That’s the part that catches so many boaters off guard. “Ninety-five percent of what we do is covered under a Sea Tow membership,” Frohnhoefer says. “The true salvage jobs are few and far between, but that’s where the biggest surprises happen.”

A Brief History of Maritime Salvage Law

Salvage law is one of the oldest forms of legal protection on the water, and it is an important hurricane prep topic for boat owners to understand before storm season. Dating back centuries to when sailors relied on one another for survival, the system was created to reward those who risked their own ships and lives to save property in danger at sea.

In 1869, the landmark Supreme Court case The Blackwall cemented this principle in U.S. law after a fire in San Francisco Harbor. A steam tug helped extinguish flames on a burning ship and was awarded a portion of the vessel’s saved value for its efforts—a ruling that established the idea of a “salvage award.” Since then, courts have continued to uphold the rule that voluntary, successful efforts to save a vessel in peril deserve compensation.

That same principle has echoed through modern cases, from the 2012 America’s Cup yacht rescue in San Francisco to NASA’s 1994 recovery of a drifting space shuttle fuel tank during Tropical Storm Gordon—the largest salvage award in history.

Maritime law has evolved, but the foundation remains unchanged: saving a vessel in peril is salvage, and the salvor has the right to be paid for that service.

What Insurance Covers and What It Doesn’t

This is where boaters often get blindsided. A towing membership is not an insurance policy, and most basic boat insurance doesn’t automatically cover salvage unless it’s specifically written into the policy. “You really have to look at your insurance and question your provider,” says Frohnhoefer. “You want to make sure you have proper hull coverage, that services by a third party will be covered, and not just the ungrounding or refloating, but also transport, storage, and even demolition if the vessel is a total loss.”

Policies vary widely. Some only pay a percentage of recovery costs. Others won’t pay at all if the vessel was outside its navigational limits. Frohnhoefer has seen claims denied for boats that were just a few miles south of a policy boundary line. “Different policies start and stop in different places,” he says, “so you need that full, comprehensive coverage, from the incident to the final resolution.”

Liability-only insurance is another pitfall. It may pay to recover your boat, but not to store or transport it afterward. “People end up with a sunk, unusable boat and big marina bills,” Frohnhoefer warns.

Avoiding Surprises on the Water

In a true emergency, even the best hurricane prep can be tested, and it’s easy to panic and accept help without asking questions. Frohnhoefer stresses that communication is key. “Never just say, ‘Take my line,’ without asking: Is there going to be a charge for this? What will it be? How do you intend to recover my vessel? Where are you taking it?” Ethical salvors will explain your options up front. If someone pressures you to act immediately or refuses to answer questions, those are red flags.

“When you have insurance, call your broker or claims agent,” he says. “They’ve handled this before and can guide you through it.”

Understanding why salvage bills exist also helps. Maritime law doesn’t treat it like an ordinary service call—it’s a reward system meant to encourage people to act when another vessel is in danger. “If a $500,000 boat hits something and starts taking on water, and we save it, we’re entitled to a percentage of that post-damage value,” Frohnhoefer explains. “That’s what keeps private salvors ready around the clock. We’re not tax-funded like the Coast Guard, we have to maintain boats, gear, and personnel 24/7.”

Preparing Before the Storm

Frohnhoefer’s hurricane advice is simple but vital: act early and don’t wait for the warning cone to cover your ZIP code. “Have a plan and have the proper insurance, and prepare early,” he says. “Even if you lose a weekend of boating, it’s better than waiting until the storm is three days out.”

Haul your boat out or secure it before facilities shut down and insurers stop writing new policies. Remember that if your vessel breaks loose and damages someone else’s property, you’ll likely be responsible. And don’t assume you can just “let it sink” for an insurance payout. Most policies require that you take all reasonable steps to preserve your vessel’s value, including accepting a salvor’s assistance if offered.

The Bottom Line

When disaster strikes, understanding the difference between towing and salvage should be part of every boater’s hurricane prep. It can save you from a financial disaster on top of a physical one. Sea Tow will always come to help, but if your boat is in peril, the law classifies that as salvage, and it must be covered by insurance or paid for out of pocket.

As Frohnhoefer puts it, “We’ve seen just about everything, but even I’m still surprised sometimes. Talk with your insurance provider, learn from other boaters’ experiences, and make sure you know exactly how your policy responds in real-world scenarios.”

When the next storm rolls in, the right hurricane prep plan and the right policy can be the difference between a stressful cleanup and a financial catastrophe.